AI News Today July 12 2026: 15 Biggest Stories

Apple says more than 400 of its former employees now work at OpenAI, and on July 11 it took that grievance to federal court. That lawsuit landed in the same 48 hours as a leaked Gemini 3.5 Pro launch date, the largest ADR debut in Wall Street history, and the Federal Reserve handing Marc Andreessen a policy seat. The launch-week chaos of GPT-5.6 and Grok 4.5 is not cooling off. It is compounding.

Here are the 15 stories that matter for July 12, 2026, with the numbers, dates, and caveats you need. For running coverage of every release this month, bookmark our AI industry news and trends hub.

1. Apple Sues OpenAI for Trade Secret Theft After Losing 400+ Employees

Apple filed a lawsuit against OpenAI in Northern California federal court on July 11, 2026, alleging trade secret theft and citing more than 400 former Apple employees who now work at OpenAI. According to early reports of the complaint, Apple frames OpenAI's recruitment of its silicon engineering, on-device AI, and hardware design teams not as ordinary talent movement but as a coordinated campaign to extract confidential technology. The 400-plus figure is the headline number, and it is a staggering one: that is not a handful of defections, it is an entire division's worth of institutional knowledge walking out the door over roughly two years.

The context makes the filing feel almost inevitable. OpenAI has spent 2026 hiring aggressively at the most senior levels of the industry, including Gemini co-lead and Attention Is All You Need co-author Noam Shazeer from Google DeepMind on June 18, and it has been building consumer hardware ambitions since acquiring Jony Ive's io. Apple, meanwhile, has spent the same period fielding criticism that Siri and Apple Intelligence have fallen two full generations behind frontier assistants. When you are losing both the product race and the people who could win it for you, the courtroom becomes the remaining venue. The complaint just landed and the specific trade secrets at issue are still redacted or unspecified in public reporting, so treat any characterization of the claims' strength with caution.

What happens next matters for the whole industry. If Apple wins early procedural fights or forces broad discovery into OpenAI's hiring practices, every frontier lab that has been raiding Big Tech for silicon and systems engineers will have to slow down and paper its recruiting far more carefully. And the timing could not be worse for OpenAI: a trade secret suit from the world's most litigious hardware company is exactly the kind of legal overhang IPO bankers hate, weeks before a planned confidential filing. My take: this is the first big lawsuit of the AI talent-war era, and it will not be the last. Poaching at this scale was always going to end up in front of a judge eventually.

2. OpenAI Preps Confidential IPO Filing at a $730 Billion Private Valuation

OpenAI is preparing a confidential IPO filing with Goldman Sachs and Morgan Stanley, targeting a public debut as soon as September 2026 at a private-market valuation around $730 billion. If it prices anywhere near that number, it becomes the largest technology IPO in history by a wide margin, and one of the defining market events of the decade. The company has been assembling the machinery for months: TechCrunch reported in June that OpenAI was bringing on senior finance and policy heavyweights ahead of a listing, and on July 6 it hired Dean Ball to lead a new Strategic Futures team reporting directly to Chief Strategy Officer Jason Kwon.

The uncomfortable backdrop is competitive, not procedural. Fortune reports that Anthropic has overtaken OpenAI on revenue, running at roughly $47 billion annualized against OpenAI's projected $25 to $33 billion for 2026. Anthropic's enterprise engine is a big part of that gap: Claude Code alone went from $1 billion in annualized revenue at the end of 2025 to more than $2.5 billion by February 2026, and the company leads on developer market share and agentic coding reliability. An IPO forces OpenAI to publish audited numbers for the first time, and those numbers will be read side by side with a rival that monetizes enterprise workloads better per user.

None of this means the IPO fails. OpenAI still owns the biggest consumer AI brand on the planet, ChatGPT's distribution moat is real, and the GPT-5.6 launch gives bankers a fresh growth story to sell. But between the Apple lawsuit in story 1, Anthropic's revenue lead, and a $730 billion sticker that demands flawless execution, September 2026 is shaping up as the most scrutinized listing since the dot-com era. Every AI builder should watch the S-1 when it goes public: it will be the first honest look inside the unit economics of frontier AI.

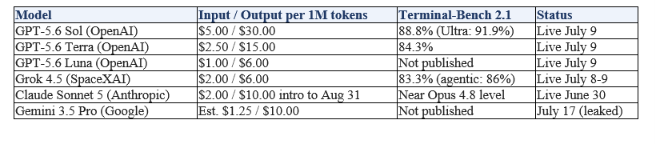

3. GPT-5.6 After 48 Hours: Terra Is the Value Pick and Sol Hits 750 Tokens Per Second

Two days after the July 9 launch, the developer consensus on OpenAI's three-tier GPT-5.6 family is settling into a clear shape: Terra is the value pick, Sol is the benchmark king, and Luna is the budget workhorse. GPT-5.6 Terra, priced at $2.50 input and $15 output per million tokens, scores 84.3% on Terminal-Bench 2.1, roughly matching Claude Fable 5 at about half the cost. Sol, at $5 and $30, posts 88.8% standard and a field-leading 91.9% in its Ultra configuration. Luna, at $1 and $6, has no published Terminal-Bench score yet but is already absorbing high-volume, low-stakes workloads like classification and summarization across early API deployments.

The infrastructure story is arguably bigger than the benchmark story. Sol served on Cerebras wafer-scale hardware is hitting 750 tokens per second, against the 30 to 80 tokens per second typical of GPU-based serving. That is not an incremental speedup, it changes what you can build: agent loops that took minutes now take seconds, and long-document workflows stop feeling like batch jobs. Sam Altman also claims Sol is 54% more token efficient on coding tasks than its predecessors. That number came from OpenAI's own materials, not independent testing, so run it against your own workloads before you re-architect anything around it.

There are still open questions the community is actively probing, including the Luna-Terra benchmark paradox flagged by early testers, where Luna occasionally outperforms Terra on specific reasoning suites despite its lower tier and price. Alongside the models, OpenAI shipped ChatGPT Work, its agentic productivity product that merges Codex into the ChatGPT desktop app with a 15-integration plugin directory. The launch-day details, including how ChatGPT Work stacks up against Anthropic's Claude Cowork response, are in our July 10 AI news recap. The bottom line after 48 hours: OpenAI priced this family to win back API market share, and the early developer chatter suggests it is working.

4. Gemini 3.5 Pro Finally Has a Date: July 17

Google DeepMind's Gemini 3.5 Pro is set for general availability on July 17, 2026, according to a leaked launch plan that circulated on July 10. The specs, if they hold, are genuinely aggressive: the model was reportedly rebuilt on an entirely new pretraining run rather than adapted from 2.5 Pro, ships a 2-million-token context window (double anything in the current frontier field), and gates its Deep Think extended reasoning mode behind the $250 per month Ultra subscription. Expected API pricing sits around $1.25 input and $10 output per million tokens, which would undercut GPT-5.6 Sol by 4x on input cost while doubling everyone's context.

The delay is the subtext every developer already knows: Gemini 3.5 Pro is now six weeks late, and it lands into the most competitive single week in AI history, five days after GPT-5.6 and nine days after Grok 4.5. Google has also spent the intervening weeks absorbing painful talent news, with Noam Shazeer departing for OpenAI and Nobel laureate John Jumper leaving for Anthropic in June, moves that prompted Fortune to openly question whether DeepMind can stay at the front of the race. A great model on July 17 quiets all of that. Another slip, or a model that merely matches Sol, does not.

My read: the pricing is the tell. Google is not trying to win the benchmark headline, it is trying to win the workload migration. At $1.25 input with 2 million tokens of context, entire categories of RAG architecture get simpler because you can just put the corpus in the prompt. Where every current model stands before the July 17 scramble is on our best AI models July 2026 leaderboard, and we will re-rank the field the day Gemini 3.5 Pro ships.

Don't just use ChatGPT. Learn to build custom LLM agents, RAG pipelines, and full-stack Agentic AI apps in our intensive 6-week program.

5. Google Search Is Now Fully Gemini 3.5 Flash

As of July 10, Google Search results are entirely powered by Gemini 3.5 Flash generated summaries, replacing the traditional ten blue links format across the board, with source links embedded inside the AI-generated page rather than listed separately. This is the full rollout of the format Google has been testing in stages since AI Overviews launched in 2024, and it means the default experience of the world's most-used website is now a generated document, not a ranked index.

It is hard to overstate what this does to the web's traffic economy. For twenty-five years, the implicit contract was that publishers produced content, Google ranked it, and clicks flowed downstream. That contract is now gone: visibility means being cited inside the AI answer, not ranked beneath it. Publishers and SEO teams have watched referral traffic erode for two years, but a fully generated results page converts erosion into a structural cliff. Expect the antitrust and publisher-compensation fights, already simmering in the EU and US, to escalate sharply from here.

For anyone who publishes anything, the practical playbook changes today: answer-engine optimization and generative-engine optimization stop being buzzwords and become the whole game. Content that is entity-rich, directly quotable, and structured for extraction gets cited; content optimized for the old click economy becomes invisible. Hot take: within a quarter, being quotable will matter more than being rankable, and the sites that adapt first will own a disproportionate share of AI-referred traffic for years.

6. SK Hynix Pulls Off the Largest ADR Debut in History

SK Hynix began trading on Nasdaq under ticker SKHY on July 10, 2026, with its $28 to $29 billion ADR offering priced at $149 to $166 per share, surpassing Alibaba's 2014 debut of $21.8 billion as the largest ADR listing in history. The numbers underneath the listing explain the appetite: SK Hynix holds roughly 60% of the global high-bandwidth memory market, and it posted Q1 2026 revenue of $35.55 billion at a 72% operating margin. For a memory company, a segment that spent decades as the most brutally cyclical commodity business in tech, a 72% operating margin would have been science fiction three years ago.

HBM is the reason. Every frontier training cluster and every high-end inference deployment needs high-bandwidth memory stacked next to the accelerator, and Nvidia's entire data-center roadmap is gated on HBM supply. SK Hynix beat Samsung and Micron to each successive HBM generation, locked in the Nvidia qualification wins, and turned memory into a sole-source-like business with pricing power to match. The US listing gives American institutional money direct access to that position at the exact peak of AI memory demand, without the friction of the Seoul exchange.

The strategic signal matters as much as the money: the AI supply chain is consolidating its capital access in New York. Between this debut and the broader chipmaker rally in story 7, the market is saying loudly that it currently trusts hardware margins more than model-layer margins. If you want a single stock chart that summarizes the 2026 AI economy, SKHY's first week of trading is a good candidate.

7. Nvidia Reclaims $5 Trillion as Chipmakers Win the Quarter

Nvidia rose 2.3% on Friday July 10 to push its market capitalization back above the $5 trillion mark, capping a week in which semiconductor names broadly outperformed the AI software companies they supply. Microsoft, Tesla, and Amazon posted modest gains alongside, while Meta jumped more than 7% on its compute expansion memo (story 8). The quarter's scoreboard is unambiguous: the chipmakers won it.

The pattern deserves attention because it has now repeated for several consecutive quarters. Model launches dominate headlines, GPT-5.6 and Grok 4.5 each owned multiple news cycles this month, but the durable cash keeps landing one layer down, in accelerators, high-bandwidth memory, advanced packaging, and power infrastructure. Frontier labs compete each other's margins away with weekly price cuts (Grok 4.5 at $2 and $6, Terra at $2.50 and $15, Gemini 3.5 Pro reportedly coming in at $1.25 and $10), while every one of those price cuts requires buying more silicon to serve more demand. Price wars at the model layer are revenue growth at the chip layer.

SK Hynix's record ADR debut and Nvidia's round number landing in the same week is not a coincidence. It is the market repricing picks and shovels, again, and it is a useful sanity check for builders: the companies selling compute have visible, compounding economics, while the companies selling intelligence are still discovering what their pricing power actually is.

8. Meta Memo: Double Compute by 2027 and a $10 Billion Canadian Data Center

Meta stock surged more than 7% intraday on July 10 after an internal memo revealed plans to sign long-term supplier agreements, including with Samsung, aimed at doubling the company's total compute capacity by 2027. In the same news cycle, Meta announced a $10 billion investment to build a 1-gigawatt data center in Alberta, its first facility in Canada and its 33rd data center globally. Taken together, the two announcements are Meta's loudest statement yet that it intends to stay a frontier lab rather than become a distribution partner for someone else's models.

The Samsung angle is worth dwelling on. Diversifying long-term supply agreements beyond the usual Nvidia-TSMC-SK Hynix axis gives Meta leverage in the exact market where SK Hynix's 60% HBM share (story 6) has concentrated pricing power. And the Alberta site continues the industry's migration toward jurisdictions with cheap power, cold climates, and fast permitting: a 1-gigawatt campus is a small city's worth of electricity, and those deals are increasingly won at the provincial level, not the federal one.

Investors have also been chewing on reports that Meta plans to sell surplus AI compute capacity to external customers, a business that would put it in direct competition with the hyperscaler clouds for the first time. The 7% pop says the market likes the aggression. The open question is the one every lab faces in 2026: whether doubling compute doubles anything measurable on the revenue line, or whether Meta is buying optionality at $10 billion a site. Either way, the capex supercycle has no brakes.

9. Meta's Iris Chip Enters Production in September

Meta plans to begin manufacturing its custom AI processor, code-named Iris, in September 2026 after completing initial testing. The chip is designed in partnership with Broadcom and will be manufactured by TSMC, and reporting is explicit that Iris is intended to complement rather than replace the large volumes of GPUs Meta continues to buy from Nvidia and AMD. Iris will carry internal AI infrastructure workloads, the recommendation and ranking systems plus a slice of inference, where a custom part tuned to Meta's own models beats a general-purpose GPU on cost per query.

With Iris, the hyperscaler custom-silicon club is now complete. Google has TPUs in their seventh generation, Amazon has Trainium, Microsoft has Maia, and OpenAI unveiled its Broadcom-built Jalapeno inference chip earlier this year. Broadcom, notably, is designing for several of these programs simultaneously, which has quietly made it the second most important company in AI silicon after Nvidia itself. The playbook is the same everywhere: move the predictable, high-volume inference workloads onto in-house parts, keep buying Nvidia for frontier training, and use the credible threat of internal silicon as a negotiating lever on every GPU purchase order.

That last point is the honest way to read Iris: the strategic goal is negotiating leverage against Nvidia, not independence from it. No hyperscaler custom chip has yet displaced Nvidia from training, and none of these companies claims it will. But at Meta's inference scale, even shifting 20 to 30 percent of serving costs onto a cheaper internal part is billions of dollars a year, and September is when we find out whether Iris actually ships on schedule.

10. US Clears License-Free AI Chip Exports to the UAE

The US Commerce Department removed the United Arab Emirates from its restrictive export-control country groupings and reclassified it as A:5, permitting license-free exports of advanced AI chips to the Gulf state. The change directly benefits companies with major UAE buildouts and partnerships, with reporting specifically naming Amazon, Apple, and xAI among the winners. What previously required case-by-case licensing, with all the delay and political risk that entails, is now a routine commercial transaction.

This is the Gulf compute corridor going official. The UAE has spent two years positioning itself as the neutral ground of the AI buildout: sovereign wealth capital through MGX and G42, cheap energy, and a willingness to build at speeds US permitting cannot match. The A:5 reclassification removes the last regulatory friction between American chip supply and Emirati capital, and it slots into the administration's broader pattern this summer of loosening AI trade restrictions on allied and partner states while keeping the wall up against China.

The second-order effect to watch: frontier-scale training capacity outside US borders. Between Colossus-class clusters at home (story 15) and license-free Gulf deployments abroad, the geography of compute is diversifying fast, and with it the question of whose jurisdiction actually governs frontier training runs. Export policy is quietly becoming AI safety policy, and this week the policy got looser, not tighter.

11. The Federal Reserve Puts Marc Andreessen on Its New AI Task Force

The Federal Reserve has appointed a16z co-founder Marc Andreessen to co-lead a new task force studying AI's impact on jobs, productivity, and monetary policy, in news that broke July 11. It is the first time the Fed has formally structured a body around AI-driven economic effects, and it signals that the central bank now treats AI-related labor displacement and productivity shifts as inputs to interest-rate policy rather than as a distant research topic.

The substance matters because the macro data has turned genuinely ambiguous. Productivity numbers are strong, but white-collar hiring in exposed categories has been softening all year, and nobody at the Fed can currently say how much of either trend is AI. A task force that produces credible measurement, how much displacement, in which sectors, how fast, would give monetary policy its first real instrument panel for the AI economy. Whatever this body publishes will shape how Washington reads every AI jobs headline in 2027.

And then there is the choice of co-lead. A venture capitalist with billions invested across AI companies, whose firm's portfolio directly benefits from accommodative policy toward AI deployment, co-leading the central bank's analysis of that same technology is a genuinely unprecedented arrangement, and the conflict-of-interest questions write themselves. Supporters will say you want practitioners, not academics, reading this data. Critics will say the fox is now consulting on henhouse architecture. Both are right, which is exactly why this appointment will stay controversial for as long as the task force exists.

12. Humanoid Robot IPO Week: Agility SPAC, Unitree Shanghai, Tesla Optimus Factory

Three humanoid robotics companies moved toward public markets in a single week: Agility Robotics filed to go public via SPAC at a $2.5 billion valuation, China's Unitree cleared its Shanghai IPO, and Tesla began converting a production line into a dedicated Optimus factory. After two years of viral demo videos and pilot deployments, humanoid robotics is having its capital-markets moment, and the week's clustering is no accident: everyone wants to price before the first mover sets the multiple.

Each of the three represents a different bet. Agility is the warehouse-labor pure play, with its Digit robot already running pilots in logistics facilities and a SPAC structure that gets it public fast while the category is hot. Unitree is the manufacturing-scale bet, already the world's highest-volume producer of quadruped robots, with Shanghai listing rules that reward hardware companies with real revenue. Tesla's factory-line conversion is the most consequential of the three even without a listing attached, because Optimus economics only work at automotive production scale, and converting a line is the first irreversible physical commitment to that scale.

The caveat worth stating plainly: none of these companies has demonstrated humanoid unit economics that close at scale. Bill-of-materials costs, field reliability, maintenance burden, and the actual labor-replacement rate in production settings are all still closer to pilot data than to proven business. Public listings will force the industry to publish real deployment and margin numbers for the first time, and that transparency cuts both ways: it will either validate the category and unlock the next capital wave, or deflate it fast. Either outcome is better than the demo-video era we are leaving.

13. Mistral Ships a Robot Brain That Navigates With One Cheap Camera

Mistral released a robotics navigation model that lets a robot find its way through real environments using a single low-cost camera, with no lidar, depth sensors, or expensive multi-camera rigs required. It is the French lab's most concrete move yet into embodied AI, and the framing is classic Mistral: take a capability the big labs bundle into expensive vertical stacks, and ship it as an efficient, accessible component. Monocular navigation at commodity-camera prices attacks the single biggest cost line in small-robot autonomy.

The economics are the point. A capable navigation stack built on lidar and depth hardware can cost more than the rest of a small robot combined, which is a large part of why autonomous mobile robots remain a premium product. If a single webcam-class sensor plus a learned model can do the job to production reliability, the addressable market for autonomous anything, from warehouse tugs to inspection robots to consumer devices, expands by an order of magnitude. It also positions Mistral, which lacks the robot fleets of a Tesla or the capital of a DeepMind, as an arms supplier to everyone else's embodiment efforts.

The honest caveat comes from this week's research literature, which kept landing on the same catch: locomotion and navigation are getting solved, but models keep losing basic world knowledge the moment you fine-tune them to act. A robot that navigates flawlessly but no longer understands what it is looking at is not an autonomous system, it is a very good pathfinder. Cheap navigation is real progress. Robots that both move well and reason well remain unsolved, and that gap is where the next two years of embodied AI research will live.

14. HHS Deploys ChatGPT to Audit $2.1 Trillion in Medicare and Medicaid Spending

The US Department of Health and Human Services announced on July 10 that it will deploy ChatGPT to analyze audit reports from all 50 states, hunting fraud and waste across the roughly $2.1 trillion in annual Medicare and Medicaid spending. The program is led by Assistant Secretary Gustav Chiarello, and the enforcement teeth are real: findings can escalate to withholding federal funding from states. It is one of the largest single government deployments of a commercial large language model ever announced, and it makes HHS the most consequential test case for LLMs in high-stakes public administration.

The case for the program is straightforward. State audit reports are exactly the kind of sprawling, inconsistent, semi-structured document corpus that humans review slowly and LLMs summarize quickly, and improper payments across federal health programs are estimated in the tens of billions annually. If ChatGPT surfaces even a small fraction of that reliably, the program pays for itself many times over. It is also a landmark commercial win for OpenAI in the federal market, landing the same week as its GPT-5.6 launch and IPO preparations.

The risk is equally straightforward: hallucinated findings in an audit pipeline that can pull state funding is a failure mode with real victims, and HHS has not yet published its verification methodology, appeal process, or human-review requirements. An LLM flagging a pattern for a human investigator is defensible engineering; an LLM output feeding directly into enforcement is not, and which of those two systems HHS actually built is the detail every state Medicaid director now needs answered. If you are building agentic review pipelines yourself, the patterns in our open-source Gen AI cookbooks show how to put human checkpoints in front of consequential actions, which is exactly the architecture a program like this needs.

15. The Infrastructure Money Story: Colossus Rents and SambaNova's $1 Billion

The strangest economics in AI right now: Anthropic is paying roughly $1.25 billion per month for capacity on SpaceXAI's Colossus 1 cluster, Google is paying around $920 million per month for Colossus 2, and Reflection AI is in for $150 million per month, all of them renting compute from the same company whose Grok 4.5 competes directly against their own frontier models. Annualized, that is more than $27 billion of rival money flowing into SpaceXAI's infrastructure business, effectively bankrolling the training runs of the models they will spend next year benchmarking against.

Everyone involved understands the trade, and everyone is making it anyway, because capacity is the binding constraint and Colossus has it. That tells you two things at once: first, that compute scarcity is still severe enough to override normal competitive logic, and second, that owning physical infrastructure is the most defensible position in the industry, since even your fiercest rivals become your customers. It works while capacity is scarce. It gets very awkward the moment it is not, and the labs writing nine-figure monthly checks are surely building their exit ramps in parallel.

The venture market is funding the alternatives at pace. SambaNova closed a $1 billion Series F at an $11 billion post-money valuation led by General Atlantic, with BlackRock, Intel Capital, Qatar Investment Authority, T. Rowe Price, Battery Ventures, Capital Group, and Vista Equity Partners participating, and it follows Together AI's $800 million Series C earlier this month. Investors are betting that inference-focused challengers can peel high-volume workloads away from both Nvidia GPUs and rented mega-clusters. For how the models trained on all this compute actually stack up against each other, see our full Grok 4.5 hands-on review.

The July 12 Frontier Model Scoreboard

As of July 12, 2026, here is the frontier field on price and the Terminal-Bench 2.1 coding benchmark. Grok 4.5 remains the price-performance outlier and Gemini 3.5 Pro arrives July 17.

Prices move weekly right now, and launch-week benchmark claims deserve skepticism until independent evals land. For tool-by-tool guidance on which model to wire into your editor, our AI coding tools hub tracks the full stack.

Frequently Asked Questions

Why is Apple suing OpenAI?

Apple filed suit in Northern California federal court on July 11, 2026, alleging trade secret theft tied to OpenAI's hiring of more than 400 former Apple employees. The complaint frames the recruiting of Apple's silicon and on-device AI teams as coordinated extraction of confidential technology rather than normal job switching. Specific claims are still emerging from the filing, and the suit lands weeks before OpenAI's planned IPO filing.

When will Gemini 3.5 Pro launch?

Leaked launch plans put Gemini 3.5 Pro's general availability at July 17, 2026, with a 2-million-token context window, Deep Think reasoning on the $250 per month Ultra tier, and API pricing around $1.25 input and $10 output per million tokens. Google has not officially confirmed the date, and the model is already six weeks behind its originally expected window.

Is OpenAI going public in 2026?

OpenAI is preparing a confidential IPO filing with Goldman Sachs and Morgan Stanley, with a debut possible as soon as September 2026 at a private valuation near $730 billion. The Apple lawsuit and Anthropic's revenue lead (about $47 billion annualized per Fortune, versus OpenAI's projected $25 to $33 billion) are the two biggest overhangs on that timeline.

What is the cheapest frontier model right now?

On pure list price, GPT-5.6 Luna at $1 input and $6 output per million tokens is the cheapest of the new launches, while Grok 4.5 at $2 and $6 offers the strongest price-to-benchmark ratio with 83.3% on Terminal-Bench 2.1. Claude Sonnet 5's $2 and $10 introductory pricing runs until August 31, 2026, and Gemini 3.5 Pro is expected around $1.25 and $10 on July 17.

Why did SK Hynix list on Nasdaq?

SK Hynix's July 10 ADR listing under ticker SKHY raised $28 to $29 billion, the largest ADR offering in history, giving the memory leader direct access to US capital markets at the peak of AI demand. The company controls about 60% of the global high-bandwidth memory market and posted Q1 2026 revenue of $35.55 billion at a 72% operating margin.

What is the Federal Reserve's AI task force?

It is a newly announced Fed body studying AI's impact on jobs, productivity, and monetary policy, co-led by a16z co-founder Marc Andreessen per July 11 reports. It marks the first formal Fed structure dedicated to AI-driven economic effects, and Andreessen's extensive AI investments have already made the appointment controversial.

Recommended Blogs

Resources and Community

Join our community of 70,000+ AI enthusiasts and learn to build powerful AI applications. Whether you are a beginner or an experienced developer, Build Fast with AI helps you understand and implement AI in your projects.

● Website

● Instagram (@buildfastwithai)

● BFWAI Twitter (@BuildFastWithAI)

Agentic AI Launchpad 2026

A structured 6-week cohort program that takes you from AI basics to building and deploying real-world agentic AI systems. Includes live sessions, expert mentorship, project reviews, and a builder community network.

Ready to go from learning to building? Join the next cohort: Agentic AI Launchpad 2026

Free AI Resources

Access free tools, workshops, and micro-learning to keep building:

The AI news cycle will not slow down for Gemini week. Follow Build Fast with AI for tomorrow's 15 stories, and subscribe so the recap lands before your standup.

References

● Anthropic revenue lead (Fortune)

● SambaNova funding (Crunchbase)

● Meta compute rally (BigGo Finance)